Calculating your true Property investment returns is rarely as simple as subtracting your purchase price from your selling price. Let’s paint a picture that happens every single day in the Indian real estate market. You bought an apartment ten years ago for ₹50 lakh. Fast forward to today. The market is booming, and you just sold it for ₹1.3 Crore. Sitting at your dining table, you stare at the bank notification. You feel like a financial genius. In your head, you simply subtract 50 from 130, and voila—you made a cool ₹80 lakh profit. Time to plan that luxury international trip, upgrade your car, and maybe park the rest in a fixed deposit, right?

Not so fast. Take a deep breath. That gross number looks phenomenal on paper. However, the actual cash you get to walk away with is far lower. What you see before the government, the housing society, and the brokers take their cut is merely an illusion. Consequently, by the time you decode the taxes, hidden fees, and unavoidable legal charges, that ₹80 lakh might look closer to ₹45 or ₹50 lakh.

Swallowing this bitter pill proves difficult for many homeowners. Yet, understanding the math remains the only way to make smart financial decisions. If you want to truly understand your Property investment returns, you must look beyond the top line. Let’s rip the band-aid off. Let’s dissect exactly where all your hard-earned money actually goes.

The Illusion of Gross Property Investment Returns

People love discussing the top line when talking about real estate. “I bought it for X, I sold it for Y.” It is a simple and satisfying narrative. But the real profit you walk away with differs greatly from the basic difference between the buying and selling price.

Therefore, you must account for the erosion of your capital at multiple stages. Think of your profit like a block of ice sitting out in the Bangalore summer. It melts from all sides. For instance, taxes, brokerages, society charges, and legal fees all take a massive bite. To accurately calculate your net Property investment returns, you need to break down these melt-points one by one. Ignoring them means you are lying to yourself about how much money you actually made.

Step 1: Establishing the True Base Cost

To find your true profit, you first need to determine your actual taxable gain. The government does not simply tax the difference between your purchase price and sale price. Instead, they acknowledge that inflation eats away the value of money over time. Therefore, they allow you to inflate your purchase price using the Cost Inflation Index (CII).

The Magic of Indexation on Property Investment Returns

This process is called indexation. It reduces your taxable profit significantly. For example, if you bought a property for ₹50 lakh ten years ago, the indexed cost might balloon to ₹85 lakh today. Consequently, your taxable Long Term Capital Gain (LTCG) shrinks from ₹80 lakh to ₹45 lakh. This indexation benefit is crucial for maximizing your Property investment returns over a long holding period. It rewards you for holding onto your asset through the inflationary years.

The Budget 2024 Twist

However, the Union Budget 2024 threw a curveball. For properties acquired after July 23, 2024, the government removed the indexation benefit. In its place, they reduced the LTCG tax rate to 12.5%. Conversely, for properties bought before this date, you have a choice. You can calculate tax using the old regime (20% with indexation) or the new regime (12.5% without indexation). You must pick whichever results in a lower tax outgo. This choice drastically impacts your final wealth. Therefore, always consult a chartered accountant before filing your returns.

Step 2: Deducting the Ghosts of Purchases Past

Many sellers forget a massive expense from the past. When you originally bought the property, you paid a hefty stamp duty and registration fee. Karnataka property registration charges typically run between 5% and 7% of the property value. If you paid ₹3.5 lakh in stamp duty a decade ago, you cannot recover that money. Consequently, you must subtract this original expense from your gross profit.

Furthermore, did you pay a brokerage when you bought the property? Did you take a home loan and pay processing fees? All these initial costs add up. You must factor them into your base cost to find your true returns. Overlooking these initial outlays artificially inflates your perceived profit.

Hidden Costs That Drain Property Investment Returns

Selling a property is not free. In fact, the outgoing expenses during a sale can quickly drain your expected windfall. Let’s look at the common culprits that eat into your bottom line.

Brokerage and Marketing Costs in Bangalore

Unless you sold your property entirely through word-of-mouth, you paid a brokerage. In the Bangalore property market, brokerage typically ranges from 1% to 2% of the sale price. On a ₹1.3 Crore sale, you lose ₹1.3 lakh to ₹2.6 lakh instantly. Next, consider the staging and marketing expenses. You spent money making the house look presentable. You might have painted the walls, fixed the plumbing, or paid for premium online listings. Add another ₹50,000 for these miscellaneous prep costs. These small leaks eventually sink the ship.

Society Transfer Charges and NOCs

Many sellers get a rude shock when their housing society hands them a bill. If you live in a registered society, they will charge you a transfer fee. This fee allows them to change the ownership to the buyer’s name. Legally, societies can charge a maximum of ₹25,000. However, premium societies often levy much higher “donations” to issue the No Objection Certificate (NOC). As a result, these hidden costs can easily eat up another ₹50,000. Any comprehensive Home selling guide Bangalore will tell you to query your society about these charges before listing your property.

Legal and Documentation Fees

Furthermore, you hired a lawyer to ensure the sale runs smoothly. They draft the sale agreement, verify the buyer’s loan documents, and handle the complex stamp duty registration. Legal fees for an Apartment sale Bangalore range from ₹30,000 to over ₹1 lakh. The exact cost depends on the title’s complexity and the lawyer’s pedigree. Skimping on a good lawyer often leads to disasters later. Thus, always budget for solid legal help.

Taxes That Shrink Your Property Investment Returns

Here comes the biggest chunk of your profit vanishing into thin air—Capital Gains Tax. When you sell a property, the government taxes the profit you make. The tax rate depends entirely on how long you held the asset.

Short-Term vs. Long-Term Gains

Did you sell the property within 24 months of purchasing it? If so, you incur Short-Term Capital Gains (STCG). The government adds this profit to your total income. They tax it according to your income tax slab. This rate can hit a staggering 30% (plus surcharges and cess). Therefore, flipping properties quickly usually results in terrible Property investment returns because the taxman takes a massive bite.

On the other hand, hold the property for more than 24 months, and you benefit from Long Term Capital Gains (LTCG) rules. As discussed earlier, the rate is either 20% with indexation or 12.5% without indexation. Calculating this correctly is the most critical step in determining your Property sale profit Bangalore. Choosing the wrong tax regime can cost you lakhs.

TDS and Its Immediate Impact

The government does not wait for you to file your annual returns to get its share. Are you selling a property worth more than ₹50 lakh? The law mandates the buyer to deduct 1% of the sale price as TDS (Tax Deducted at Source). The buyer must deposit this directly with the government. So, on a ₹1.3 Crore sale, ₹1.3 Lakh vanishes before you even see the full amount in your bank.

Understanding Flat sale tax Bangalore rules is crucial. If the buyer fails to deduct or deposit this TDS, you could face harassment from the income tax department. Thus, always ensure the buyer provides you with Form 16B. This form confirms the TDS deposit against your PAN card. Never take the buyer’s word for it; demand the documentation immediately.

Outstanding Dues and Property Tax Karnataka

Before you calculate your final windfall, clear your outstanding liabilities. Did you have a pending Property tax Karnataka bill? The buyer will demand a clearance certificate. Unpaid property taxes, pending electricity bills, and society maintenance dues will all be deducted from your sale proceeds at the time of registration. Make sure you clear these well in advance to avoid last-minute scrambles.

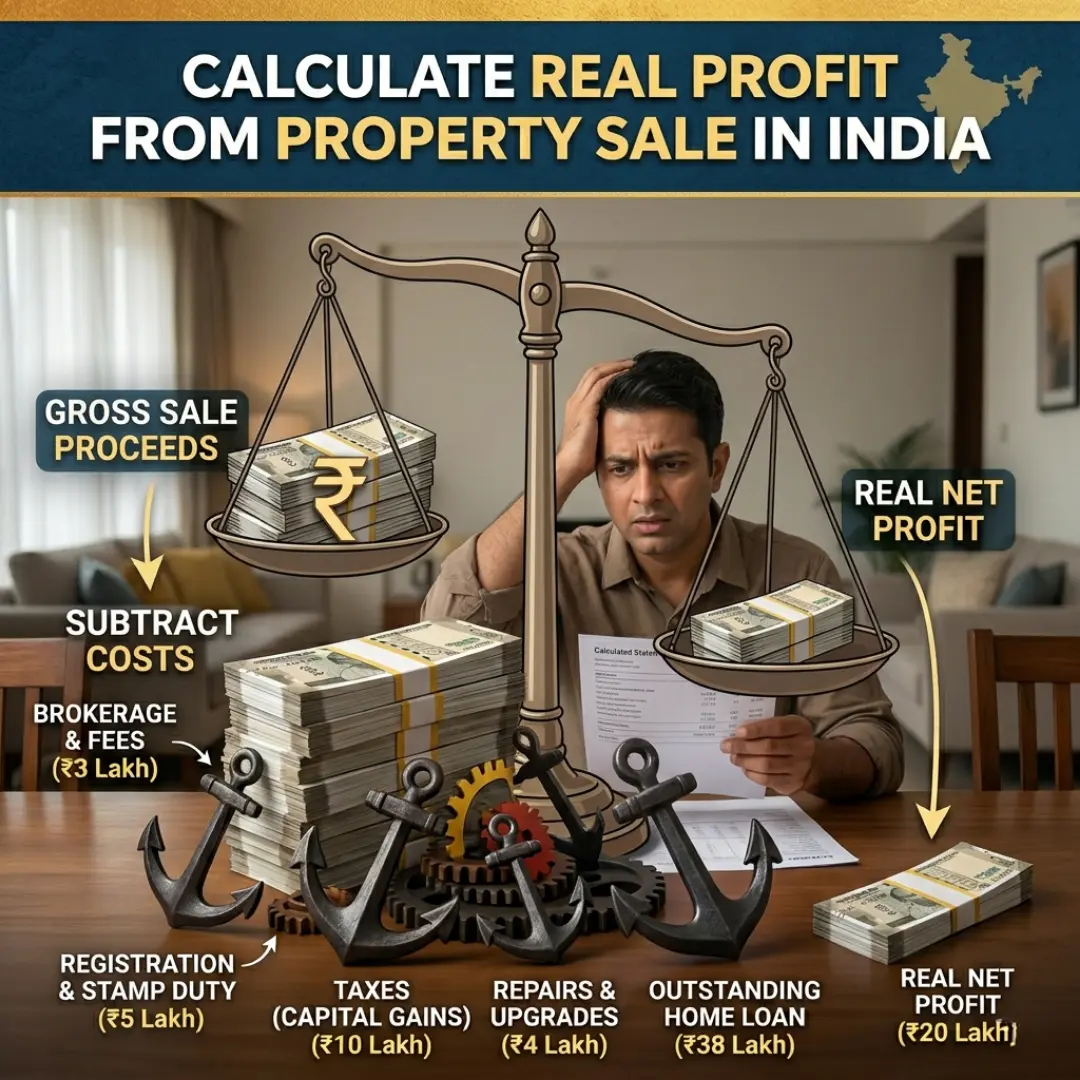

Let’s Do the Real Math: A Case Study

Now, let’s go back to our original scenario to find the true profit.

- Original Purchase Price (10 years ago): ₹50 Lakh

- Sale Price Today: ₹1.3 Crore

- Gross Profit (Illusion): ₹80 Lakh

Let’s apply reality. We will assume you opt for the old tax regime (20% with indexation) because it benefits older properties. The Cost Inflation Index (CII) inflates your purchase price. Let’s say the indexed cost becomes ₹85 lakh.

Thus, your taxable LTCG is now: ₹1.3 Crore – ₹85 Lakh = ₹45 Lakh. Tax at 20% + 4% cess = roughly ₹9.36 Lakh.

Subsequently, subtract the other charges:

- Brokerage (2%): ₹2.6 Lakh

- Society & Legal Fees: ₹1 Lakh

- Pre-sale renovation: ₹0.5 Lakh

- Original Stamp Duty: ₹3.5 Lakh

- Total deductions (Tax + Fees + Past Costs): ₹9.36 Lakh + ₹2.6 Lakh + ₹1.5 Lakh + ₹3.5 Lakh = ₹16.96 Lakh.

Your true profit reality: ₹80 Lakh – ₹16.96 Lakh = ₹63.04 Lakh.

Ouch. That is nearly ₹17 lakh less than what you thought you made. This is why understanding the math is so vital. When you know the real numbers, you can plan your financial future accurately.

The Bangalore Reality Check

Real estate is highly localized. The numbers we discussed above apply generally across India, but the specific dynamics of the city matter immensely. Currently, the Bangalore real estate trends show a massive surge in property values. The IT boom, the development of the metro, and the influx of multinational companies have pushed prices to record highs.

Therefore, Property appreciation Bangalore often outpaces many other Indian cities. A property bought for ₹50 lakh a decade ago might easily fetch ₹1.3 or even ₹1.5 Crore today, especially in prime IT corridors. However, with high appreciation comes higher capital gains taxes and larger brokerage payouts in absolute terms. Consequently, while the gross numbers look incredibly tempting in Bangalore, the net percentage of profit often tells a slightly more grounded story.

If you are planning a Real estate investment Bangalore, you must factor in these high exit costs before you even buy the property. Smart investors calculate their anticipated tax liability and selling costs before they sign the initial purchase agreement. They know that a high sale price does not always equal high net wealth if the exit costs eat up the margin.

How to Safeguard Your Property Investment Returns

Knowing that taxes and fees take such a massive bite, what can you do? How do you protect your wealth? Fortunately, the Indian Income Tax Act provides several legitimate avenues to save on taxes.

Section 54: Reinvest in Residential Property

Are you selling a residential property? You can claim an exemption on the LTCG. You just need to reinvest the capital gain amount into buying or constructing another residential property in India. You get a window of one year before or two years after the sale to buy. You have three years to construct. This strategy keeps your money working for you, generating future returns without losing a chunk to taxes.

Section 54EC: Capital Gains Bonds

Alternatively, don’t want to buy another house? Invest your capital gains in specified bonds instead. The National Highways Authority of India (NHAI) or the Rural Electrification Corporation (REC) issue these. The lock-in period is 5 years. The maximum investment limit is ₹50 lakh. Thus, this saves you tax while offering a safe, fixed return.

Buy Right to Maximize Property Investment Returns

Ultimately, you can negotiate brokerage and optimize your taxes. But the single biggest factor dictating your final bank balance is the intrinsic value and appreciation of the asset itself. You must ensure you buy a property that appreciates faster than the market average. As a result, this robust appreciation absorbs the shock of taxes and fees, leaving you with a substantial net profit.

The Strategy of Buying Right

Therefore, the best way to maximize your real profit is simple. Buy an asset with robust, undeniable growth potential from day one.

For example, if you buy a poorly located, low-quality apartment, your appreciation will barely beat inflation. After paying the heavy exit costs, you might end up with a negligible real return. Conversely, invest in a premium, strategically located project by a reputed builder. The appreciation will be so robust that even after all taxes and hidden charges, you walk away with a fortune. Quality real estate acts as a hedge against both inflation and taxation.

This is exactly why who you buy from matters just as much as what you buy. You need a developer who understands the pulse of the market. You need a developer who builds in growth corridors before they explode in value.

Why Globes Properties Bangalore Changes the Game

This is precisely where Globes Properties Bangalore steps in. We don’t just sell apartments. Instead, we curate wealth-generating assets for our clients.

When you want a home that doubles as a brilliant financial investment, you need a partner who understands market nuances. Undoubtedly, Globes Properties real estate stands renowned for its commitment to quality, prime locations, and transparent dealings. We strategically position the properties we offer for exponential growth. Therefore, this ensures your future property sale yields the highest possible returns. We believe in building value, not just buildings.

Our deep understanding of the city’s infrastructure projects allows us to acquire land in tomorrow’s hotspots today. When you buy from us, you are essentially buying into our research and market foresight. This foresight is what drives extraordinary appreciation and safeguards your financial future against market volatility.

Elite Homes: Maximizing Property Investment Returns

Meanwhile, do you want to experience the pinnacle of modern living and unmatched property appreciation? Look no further than Elite Homes, our flagship project.

Elite Homes isn’t just a residential complex. Rather, it’s a lifestyle upgrade and a smart financial move. We strategically situated it in the heart of Bangalore’s most coveted growth corridor. Consequently, Elite Homes offers unparalleled connectivity to major IT hubs, premium international schools, and top-tier healthcare facilities. The project boasts world-class amenities, meticulous Vastu compliance, and luxurious finishes. From an investment perspective, it’s an absolute goldmine.

Imagine stepping out of your luxurious apartment and being just minutes away from your workplace. Imagine your children playing in safe, world-class parks. Now, imagine the value of that convenience a decade from now. As infrastructure continues to develop around Elite Homes, property values will naturally surge. This guarantees that when you eventually decide to sell, your Property investment returns will be the envy of the market. You will command a premium simply because of the address.

The Advantage of Globes Properties Projects

Furthermore, Globes Properties projects in Bangalore always deliver superior construction quality and premium land selection. Properties here historically appreciate at rates that significantly outpace the market average. Therefore, when you buy into a Globes property, you buy into a legacy of premium living and assured returns.

Whether you explore Globes Properties apartments for your family or as a pure investment, the brand guarantees peace of mind. Browse Globes Properties flats for sale and you will find we prioritize transparent pricing. As a result, that means zero hidden fees when you purchase from us. We hate hidden charges just as much as you do. We lay everything on the table so you can calculate your future profits accurately.

Securing Your Financial Future

Finally, when the time comes to sell your unit in Elite Homes a decade from now, you will command a premium price. The demand for a Globes Properties home easily offsets the taxes and fees we discussed earlier. Indeed, buyers actively seek out our brand. They know they get quality, legal clarity, and a thriving community.

Thus, always consult a comprehensive tax guide before making your next move. Speak to a trusted financial advisor. But more importantly, make sure your next purchase comes from Globes Properties Bangalore. We build homes that truly build your wealth. Secure your financial future tomorrow by making the smartest purchase today.

Trending FAQs

1. How does the buyer calculate TDS on the sale of property in India?

Does the property sale value exceed ₹50 lakh? If so, the buyer must deduct 1% of the total sale value as TDS. For example, you sell your property for ₹1.3 Crore. The buyer will deduct ₹1.3 Lakh. They deposit this with the Income Tax Department using your PAN. Furthermore, are you an NRI selling property? The TDS rate jumps much higher, up to 23.92% on Long Term Capital Gains. Therefore, always ensure the buyer provides Form 16B as proof of deposit.

2. Can I avoid paying capital gains tax when selling my apartment?

You cannot “avoid” it, but you can legally claim exemptions. First, under Section 54, reinvest the Long Term Capital Gains into buying or constructing another residential property in India within the specified time frame. The government waives the tax if you follow this rule. Alternatively, under Section 54EC, invest the gains in NHAI or REC bonds within 6 months of the sale. You can invest up to a maximum of ₹50 lakh.

3. What typical hidden costs do sellers forget about?

Sellers often forget to account for society transfer charges. Additionally, they forget brokerage fees (1-2%). Legal consultation fees for drafting the sale deed add up quickly. Moreover, home staging or renovation costs before selling take a bite. Finally, they forget the original stamp duty and registration fees paid at the time of purchase. You cannot recover those initial expenses.

4. How do I calculate the real profit from property sale?

Start with your selling price to calculate the real profit. Next, subtract the following: the original purchase price, the indexed cost of improvement, stamp duty from the original purchase, brokerage paid to sell, legal fees, society transfer charges, and the final capital gains tax liability. Therefore, the resulting number represents your true net profit. Always do this math before planning your next big purchase.

5. Did the capital gains tax rule change recently for property sales?

Yes, the Union Budget 2024 proposed significant changes. For properties acquired after July 23, 2024, the indexation benefit disappears. Instead, the LTCG rate drops to 12.5%. Nevertheless, taxpayers can choose between the old regime (20% with indexation) and the new regime (12.5% without indexation) for properties bought before this date. Pick whichever results in a lower tax outgo.

6. Why does buying from a reputed builder like Globes Properties matter for future resale value?

Reputed builders like Globes Properties real estate offer superior construction quality, clear legal titles, and prime locations. Consequently, when you decide to sell in the future, buyers willingly pay a premium for the brand name. They want the assurance of legal safety and the maintained condition of the property. As a result, this ensures your profit stays significantly higher compared to an unbranded, poorly maintained apartment.

7. What makes Elite Homes by Globes Properties a good investment?

Elite Homes combines luxury living with strategic location advantages in Bangalore. Globes Properties Bangalore develops it, guaranteeing high rental yields and strong capital appreciation. Furthermore, the project’s premium amenities and prime connectivity to IT corridors ensure consistent, high demand. Thus, this makes your future resale highly profitable and hassle-free, ultimately boosting your Property investment returns.

8. Do I have to pay capital gains tax if I sell my property at a loss?

No. If you sell your property for less than your indexed purchase price, you incur a Long Term Capital Loss (LTCL). However, you can carry this loss forward for up to 8 financial years. Therefore, you can set it off against any future Long Term Capital Gains (from property, shares, etc.), thereby reducing your future tax burden.

9. How does indexation work for properties bought before 2014?

Indexation uses the Cost Inflation Index (CII) published by the government every year. The base year was originally 1981, but the government shifted it to 2001 in 2017. If you bought a property before 2001, you can use the fair market value of the property as of April 1, 2001, as your purchase price, and then apply indexation to that value. This significantly reduces the taxable gain.

10. Is it better to invest in Capital Gains bonds or buy a new property?

It depends on your financial goals. If you want to stay invested in real estate and need a house to live in, Section 54 (buying a new property) is better. Conversely, if you do not want the hassle of managing physical property and are happy with a steady 5-6% return, Section 54EC bonds are a safer, tax-saving alternative.

For More Visit: https://globesproperties.com/

Powered By: https://mnmreality.com/

Join The Discussion